Founder and CEO of Texas Medicare Advisors - Medicare Expert | Guides clients of financial advisors into Medicare | And referral Partner for Insurance Professionals, CPA's & HR Directors

- Jason Fisher

- Jason Fisher

- Jason Fisher

- Jason Fisher

The Big C. Very few people in this world would say they have minimal connection to that horrible disease. Everyone has a cancer story within their immediate circle. There are so many types and so many different kinds of people with all kinds of different backgrounds that end up with cancer. The weak, the strong, and the average all end up with cancer fairly equally. Everyone of every race has similar odds to end up on chemo.

Let’s not be untruthful, though. There are certain risk factors that make cancer more likely, like family history, smoking, and pre-existing conditions, like adverse working or living conditions (i.e. coal mining, asbestos, mold, contaminated drinking water). Of course, some are more likely than others to come down with it at some point.

But perhaps more terrifying than the disease itself is that it’s still so random. In my circle of influence, I know of several athletes (four off the top of my head) from my university that has all had or have cancer. Only one is over 30 and all were diagnosed early to mid-20s. I know of a dear friend of my parents who got it in his mid-40s. I’ve had clients of all ages get it over time. I had a great-uncle die before I was born.

Do you care to guess who does better in responding to cancer than others? People who had cancer or critical illness plan. No question about it. Both in terms of survival rate as well as financial health, I’ve seen families utterly devastated, losing multimillion-dollar businesses, and I’ve seen low to middle-income families come out decently, considering the disaster they just had to take on, all because they had a cancer plan.

Cancer is unfortunately likely to hit you or someone in your immediate circle, and chances are it already has. Depending on what data, any one person on earth has between a 1-in-4 and 1-in-3 chance of getting some type of cancer in their lifetime. It seems silly to roll the dice on something so serious, but many do it every day.

The Cost

Most everyone talks about the cost of cancer. It’s not cheap, and it’s not because the doctors are all out to make a buck. Cancer is just such a complicated disease that takes an incredible amount of manpower, brainpower, and technology to fight such a Pandora’s Box of possibilities.

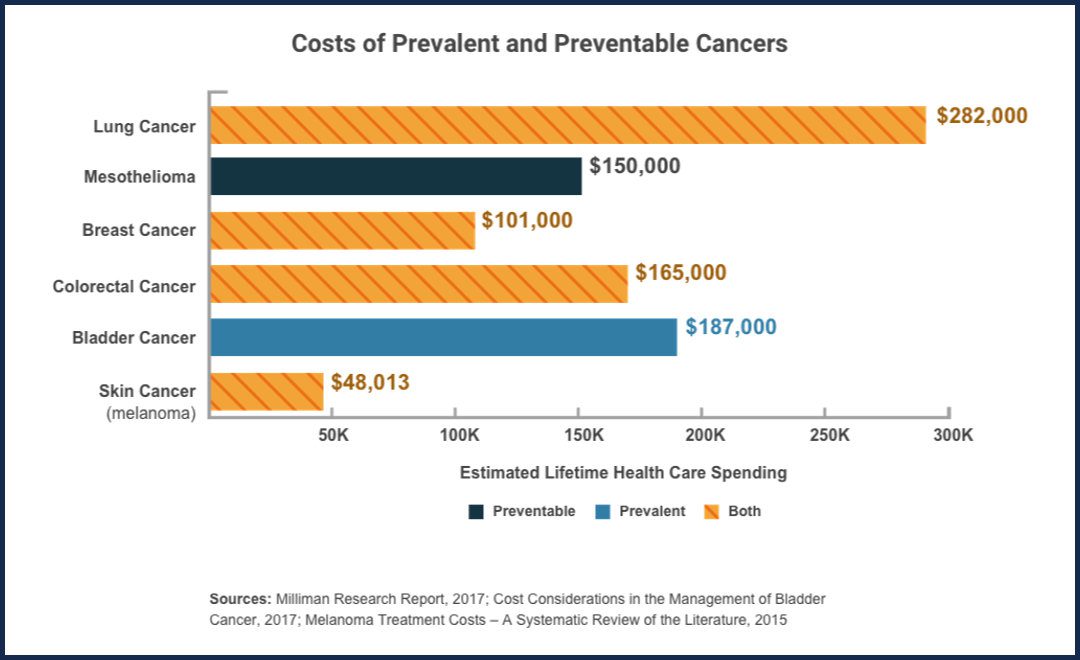

Statistics from AARP and others say the average true cost for cancer treatment is $150,000 in the US. Now that can be much less if it’s a small outpatient surgery with no follow-up, or it can be an ordeal that costs millions. Now, fortunately, there are programs that help many people that end up with a rare form that costs millions to treat. But I specifically speak to the general average today.

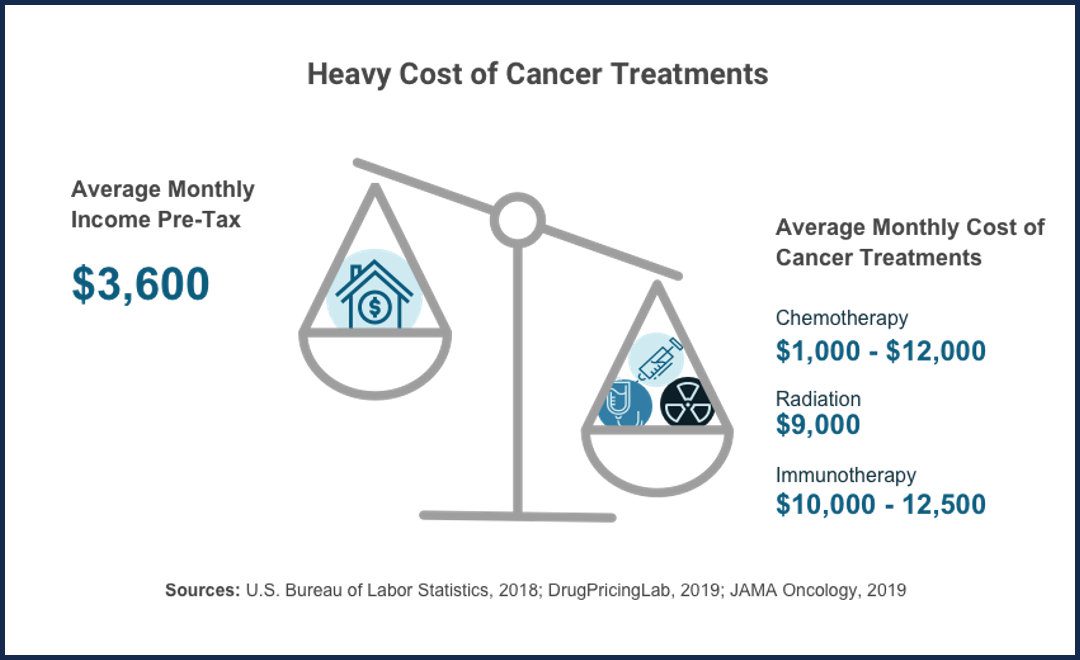

Let’s say we dip down into five figures and go up above the exact average. How do you come up with between $50,000-300,000 with no warning?

How to Pay For It

There are a few options to pay for cancer treatment. One is simply paying for it. If a cancer patient has the cash, whether it is to pay for whatever treatment within their health insurance, or whether the treatment is not covered by insurance, of course, they can just pay for whatever they need. Now, hopefully, the person has some type of health insurance, like Medicare. Even if the health insurance coverage is absolutely horrible, it will be better than having nothing. Tens if not hundreds of thousands of dollars can be saved by simply getting some kind of health coverage.

So please, if you don’t have health insurance, get it. If you can’t afford the options you know of, look around. Ask an agent. Get on Google. Something. Something is out there that may be able to help you.

The second option with cancer, especially with a rare kind, but really any kind, is getting financial assistance. Sometimes people can qualify for a more inclusive form of Medicaid that will drastically reduce or eliminate costs. But keep in mind, that is usually after having to fund it for several months or years. Others may qualify for cancer-specific programs. Others may fall under a government-funded program. Some setups are privately funded. Many experimental treatments and trials receive grants for funding. However, these are very specific. Some are just completely left out in the cold. Sometimes, you still have to pay. And most often, while waiting for payments to come, you either must wait or press forward by paying with cash or co-pay. So again, this is not a foolproof option. But of course, if someone ends up with cancer without financial protection, use the resources you have at your fingertips.

The final option for helping mitigate cancer costs is by purchasing some type of insurance plan to protect against this horrible disease. Of course, there are other ways to cover cancer with insurance, like purchasing life insurance with “Living Benefits”. In short, the idea is someone gets sick with a critical illness like cancer, and a portion of the death benefit is forwarded to the client. Of course, the subject of this article is a standalone cancer plan, but this is a really good alternative and is sometimes the best solution.

The most common way to do it is just by purchasing some cancer insurance. There are several kinds of cancer plans with all types of different designs and riders, but the two main types are cancer expense plans and cancer check plans. A cancer expense plan covers ongoing expenses for cancer treatment. For example, if you end up in the hospital, you have surgery, you receive chemo, you travel 100 miles to see the doctor, etc. You get reimbursed for your expenses up to whatever amount of coverage you have purchased each year for however long you have cancer. A cancer check idea is very simple: You pay a premium and if you ever get diagnosed with (usually) internal cancer, you get a check. For example, you pay $25 a month and you get a $25,000 check in the mail when you’re diagnosed with cancer.

In addition to cancer-only plans, it may be a great idea to look into “Critical Illness” plans, as well. These will cover cancer, but also they often cover heart attack, stroke, organ failure, transplant, and other chronic or critical illnesses. Pay attention to options for riders. Sometimes policies can offer a return of premium, ICU, ER, and hospital riders. These are all meant to be of assistance to some people.

For additional information about cancer care in Texas, click here.

Practical Thoughts

Can you go without cancer insurance? Sure. You can always choose to risk it. But do the math. Between you and your spouse, kids, and grandkids, and all of the branches around just those three generations, it is almost impossible to say someone isn’t ending up with cancer. The chances that none will throughout their lives is astronomical. The chances that several of your family or closest friends will have some type of run-in with cancer is high as well. Chances are 1-in-4 or more for one person. An average group of just four people will have a cancer patient in it.

So where do you go from here? If you have never thought about it, look into it. It is not that much to get some type of cancer coverage at any age. Some companies will offer up to $100,000 in cancer check coverage. Others offer significant riders that make it more worth your while. Cancer expense policies can be extremely helpful because they send consistent checks while receiving bills for treatment.

Don’t ignore the doctor. Don’t ignore chronic pain. Don’t ignore unexplained weight loss. Educate yourself. Ultimately, it’s about saving lives. It’s not really about the money, is it? The whole point is giving yourself the best chance to live through it by funding yourself while going through it. If cancer patient is running out of money, they’re making decisions based on what they can afford versus what they need to do to save their lives. Please don’t let that be you.

Cancer insurance gives the insured person or persons a chance to be a step ahead of those who chose not to get coverage. Don’t lose a step in a random, unpredictable fight for your life.